Following the Treasury Committee’s recommendation that the FCA be put under a ‘must have regard’ obligation for financial inclusion, the proposed legislative wording for that obligation has now been published. Sure, it’s an obligation for the FCA, not insurers. However, the assessments, planning and measures it will require the FCA to undertake will only be delivered through inputs from insurers.

Those inputs will then paint a picture about the state of financial inclusion in insurance. That will in turn drive political debate, which would in turn put insurers under pressure to explain what they're doing (or not doing) and why. What we’re seeing then is a potential window being opened onto pricing, distribution and settlement practices. Or to put it in ethical terms, how transparency will drive accountability.

Does this warrant attention before the legislator’s final decision? I think it does, for even if the proposed obligation fails this time round, the issue of financial inclusion will remain of particular interest to the influential Treasury Committee. The cross party support for the obligation points to it becoming an issue that’s going to stick around.

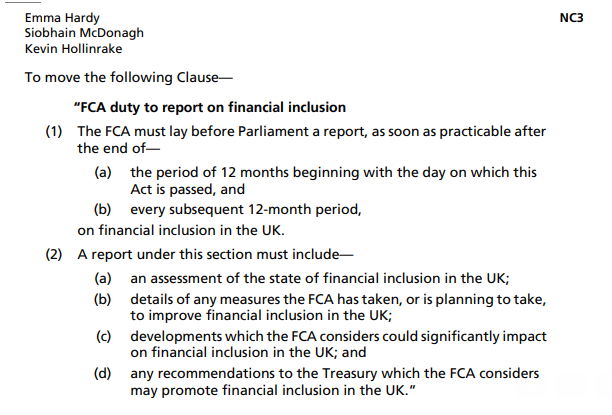

Before weighing up what insurers should consider building into their plans for 2023, let’s take a look at how exactly the obligation is being framed. Here’s how it is being worded (although this may of course change at some stage of the amendment’s progress through Parliament):

The Practical Implications

Let's explore the implications of that second clause, about what the report should include.

- An assessment of the state of financial inclusion: I would expect this to develop out of the FCA's Financial Lives Survey, the third of which was published in October 2022. Exactly to what depth 'the state of financial inclusion' assessment will be taken is unclear, but I would expect it to be on a par with the fairly detailed associated assessments in the Financial Lives Survey.

- Details of any measures the FCA has taken: this is where the politicians expect the FCA to be more proactive in drawing the line from problem to response. It is in effect amounts to an assessment of the FCA's response.

- Developments with significant impact: I think this will develop out of the Financial Lives Survey, by building on the survey's insight with more focussed foresight as to what is coming over the horizon. The intention is to push the FCA to take more preventative steps.

- Recommendations for the Treasury: while fairly obvious as a final sub-clause, it would actually push the FCA to embrace financial inclusion rather than just report on it. It will in effect be an indicator of the FCA's commitment to doing something about financial inclusion.

The Power of Transparency

In overall terms, it moves the FCA from essentially being essentially an observer of financial inclusion, to being an active player in improving it. This is what can be called the power of transparency. A reporting obligation opens the door for questions to be asked, and for answers to be expected. It focusses minds, builds expectations and facilitates accountability.

What is important to remember however, is that those expectations, that accountability, will not just rest with the regulator. Much of it will be transferred to insurers, both on an individual firm by firm basis and on a market by market basis.

I expect therefore to see the scope and depth of that reporting, if enshrined is legislation, to be hotly contested. Trade bodies and big insurers will push for it to be 'pragmatic' rather than onerous. In response, consumer groups and politicians will push for it to be meaningful and revealing. The problem for insurers is that the digital revolution happening in insurance makes reporting like this much easier to deliver than in previous semi-digital or analogue times.

The Implications for an Insurer

So what does the clause, as currently worded, mean for a typical insurer? I would expect it to lead to insurers having to...

- demonstrate how financial inclusion is factored into product and distribution strategies (the forethought),

- evidence the way in which financial inclusion is being managed in both new and existing products (the delivery)

- confirm how the three lines of defence are ensuring that the firm is working within the forethought and delivery parameters being used (the control).

Some insurers will already be doing something under each of the above bullet points. What the 'must have regard' obligation on the FCA will do is cause those existing efforts to be expanded in relation to their scope and depth, and tightened up in relation to their efficacy. Insurers should prepare for this in their plans for 2023.

Looking Ahead

There are two scenarios ahead that insurers should keep an eye on.

Firstly, the FCA doesn't really want to be under a 'must have regard' obligation on financial inclusion. This will make them reluctant applicators of the obligation if it is realised. That in turn could lead them to be less than pushy, less than thorough, on what they then expect insurers to report in turn to them.

Secondly, any indication that the regulator is not adopting the obligation full heartedly could trigger political responses in return. The simplest, but also most explosive, would be for the clause to be tweaked to require the regulator to introduce some form of benchmarking.

With a topic like financial inclusion, that would amount to a 'name and shame' list by another name. That is something the regulator hates to do, largely because it can result in outcomes that are 'two steps forward, three steps back'. That said, the cross party support amongst members of the Treasury Committee for the obligation clause points to it being a subject that isn't going to drift off their agenda. They will want to see their political support produce outcomes that meet their expectations. I hope the FCA recognises that.